We live in unpredictable times. When we wrote our Q1 outlook, few clouds appeared on the market’s horizon. The Big Beautiful Bill included a tax provision allowing for accelerated capex depreciation—a bullish development for corporate earnings. Meanwhile, inflationary pressures remained well-contained amid a softening economy—a recipe for a friendly Fed.

Then the U.S. and Israel attacked Iran, and our two bullish catalysts evaporated overnight.

With the caveat that one tweet can change things dramatically, here are 3 things investors should watch out for as we move through the second quarter.

1. Markets May be Underpricing Potentially Bad Outcomes from Iran War

The situation with respect to Iran and the Strait of Hormuz remains fluid. Whether the ceasefire holds is another question, of course, as the U.S. recently shot at an Iranian vessel attempting to cross the Strait.

More to the point, tanker traffic in this key energy corridor remains depressed. So long as this remains the case, the world faces a substantial energy deficit for which there is no quick fix. If the Strait remains mostly shut, crude oil prices could resume this ascent, with negative implications for growth (down) and inflation (up).

Curiously, though, markets have stayed sanguine about this prospect so far. Equities only suffered a mild correction (and then soared), long-term interest rates remained well behaved, and gold sold off (although central bank selling may have played a role in how bullion acted). Tumbling implied volatility in both equities and bonds serves as further indications of investor complacency.

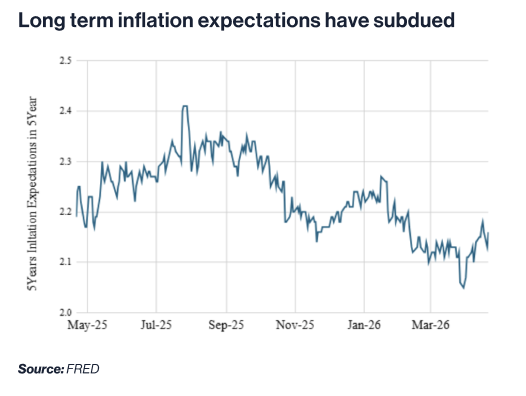

At the same time, inflation expectations have remained remarkably well-contained. The following chart shows, the 5y5y breakeven inflation rate has only increased marginally since the beginning of the war. And speaking of expectations, estimates for corporate earnings continue to be quite ebullient, despite the hit that many companies will take from higher oil prices.

We think it’s possible that cognitive dissonance may be at play in how investors have reacted to this massive energy shock. Perhaps the market isn’t willing—yet—to come to grips with how bad the energy deficit might be (emphasis on ‘might’). If so, there’s at least the possibility of a sharp repricing in equities if investors start to believe the flow of Middle Eastern oil will be disrupted for many months to come.

2. A Less Friendly Fed?

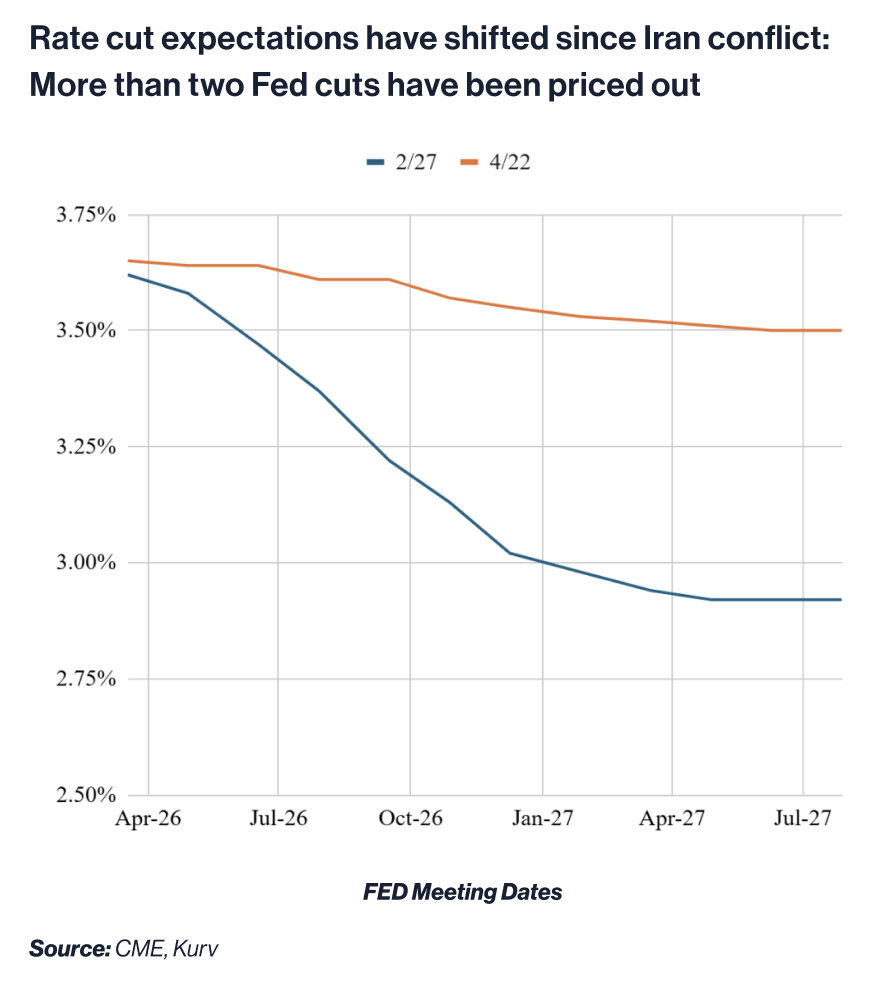

The Iran conflict may complicate the path of Fed policy. Should the oil shock persist, the FOMC could hike rates to fight inflation, or cut rates to support growth. Option one would risk tipping the economy into recession, while easing policy might threaten a resurgence of mild stagflation. Already, the market has priced out more than two cuts this year, indicating investors may be sensing the Fed won’t be as friendly as previously thought.

3. Zooming Out: Longer Term Implications of the War

It’s easy to be consumed by the near-term headlines, but investors should be mindful that the war against Iran may have longer-term implications for economic policy and asset prices. The most obvious takeaway seems to be that countries will redouble efforts at achieving energy independence.

Beyond that, we could see a resurgence of the debasement trade as the rest of the world increasingly worries about U.S. reliability. So, while the dollar has benefited from being the cleanest dirty shirt since the start of the war, this appeal may fade over time as investors diversify away from dollar assets.

The unpredictable era we live in is unlikely to give way to a sea of calm anytime soon. That means another implication of the Iran war is that volatility (and implied volatility) is likely to stay elevated in the months and years to come. Investors will need to protect their portfolios from higher structural volatility—and use this regime to harvest income when it makes sense.

Important Information:

The foregoing is general market and economic commentary prepared by Kurv investment professionals as of 04/28/2026. The commentary is neither to be construed as general investment advice nor personalized investment advice. Our commentary is subject to change based upon our views of market, economic, political and related factors. We are under no obligation to provide updated commentary if our views change. To the extent the commentary covers market segments, market sectors, industries, commodities or other securities please note that Kurv professionals may effect transactions in such market segments, market sectors, industries, and commodities or other securities which presents a conflict of interest. All Kurv investment professionals are subject to the firm’s Code of Ethics policy.

For more information on Kurv Investment Management please visit www.kurvinvest.com.