Large Cap Tech: The Long and Short (Term) of It

With any sector of the market, a key challenge for investors is to distinguish between what’s happening in the near term, and what's happening on a long-term basis. So often, people suffer from “recency bias”, extrapolating the price action in the last few weeks or months from underlying cyclical or structural trends.

Zooming In: Why There’s Been a Consolidation

Such seems to be the case with large-cap technology stocks right now. The Magnificent 7 have struggled since the start of the year. Some of this underperformance is just a function of how well they performed in 2025. Indeed, after bottoming in early April shortly following the Liberation Day stock market rout, big cap tech carried the bullish torch for U.S. indexes well into the fall. When you have such a big run, a consolidation is to be expected (and healthy, in fact). Bull markets that digest their gains have the potential to keep going once nervous longs have bailed.

Sector rotation has also clearly played a role in large cap tech’s short-run underperformance. Investors, having enjoyed great gains with tech, not surprisingly decided to redeploy some capital into less loved areas of the market. Banks and energy stocks, among others, have been the beneficiaries.

The Iran war has also presented headwinds to tech stocks (along with the overall market). Beyond being a risk-off event, the conflict has of course led to much higher oil prices. This, in turn, has fed through to higher bond yields: The 10-year U.S. government yield, which touched around 3.95% in late February, surged 30 basis points (BPS) by March 13 alongside rising oil prices. Higher long-term yields tend to weigh on tech stocks given that much of their valuations rest on expected earnings many years out.

It’s nearly impossible to predict how the Iran situation will play out. We could see easily more oil strength if the Strait of Hormuz stays closed, and this would likely pressure both risk assets and bonds—a short-term bearish concoction for large-cap tech, in all likelihood. On the other hand, if there’s a ceasefire and the Strait reopens, oil should fall, taking bond yields down. Such a development ought to be positive for tech stocks.

Zooming Out: Reasons for Optimism

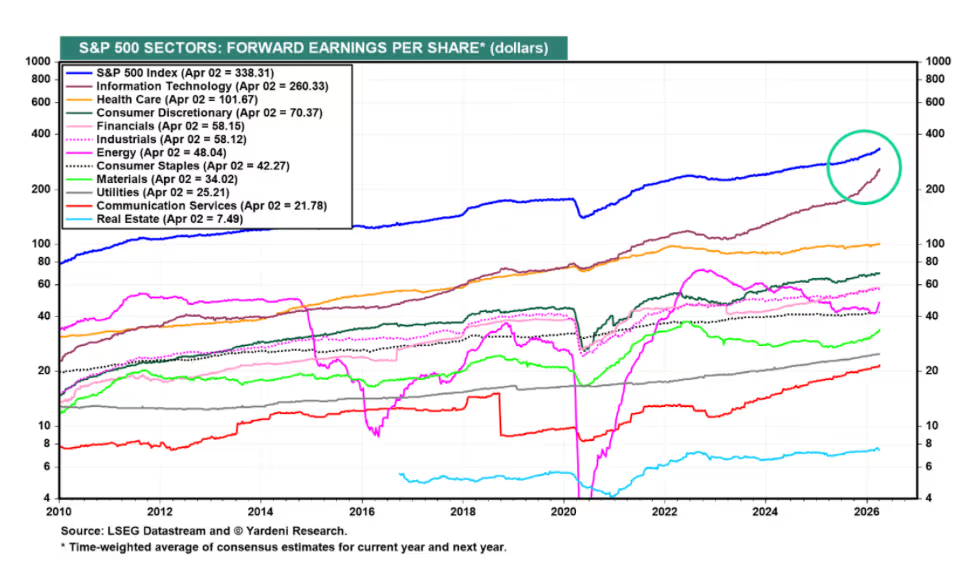

Kurv continues to see reasons to be optimistic about the long-term prospects for tech stocks—despite sometimes unpleasant downside volatility. As we have previously argued, big tech companies in the last 15 years have achieved an impressive feat: Matching the performance of broader indices on the downside, while posting better returns during up markets. This favorable risk-reward profile has been the result of big tech consistently delivering above-average revenue and earnings growth.

We are particularly bullish about the artificial intelligence buildout. In 2026, hyperscalers such as Meta, Microsoft, Alphabet, and Amazon are poised to spend nearly $700 billion in capex (capital expenditures). This spending will benefit companies that produce memory, as more powerful chips require increased levels of memory to operate. The result is an expected memory shortage, leading to higher pricing power for the suppliers of memory. So long as the hyperscalers keep spending at their current rates, the bullish case for memory stocks should remain intact.

Valuations, Valuations, Valuations

With each new headline about yet another data center buildout, investors may question whether the technology sector is too expensive. These worries are natural, especially given the run these equities have had in the last few years.

Yet valuations tell a more comforting story. The price to earnings (P/E) ratio for the technology sector has been falling since the beginning of the year. This trend accelerated with the fall in stocks brought on by the U.S.-Israel/Iran war. At its trough in April, tech had retreated to a P/E just above 20, a level not consistently seen since 2019

The lower P/E ratio is the consequence of both the price retracement in the numerator and the increase in forward earnings expectations in the denominator. While we think the market hasn’t fully priced in the inflationary impact from heightened crude oil prices, we do believe this is beginning to be an attractive entry point to a sector that has been the persistent growth engine of the U.S. economy.

KQQQ: Potential for Growth + Ongoing Income

Kurv Technology Titans Select ETF (Ticker: KQQQ) seeks to maximize total return by actively managing a portfolio with concentrated exposure to high conviction technology giants, while at the same time generating potentially tax-efficient income.

Crucially, KQQQ is not limited to the Nasdaq 100, nor those names officially classified as technology companies. This feature allows the portfolio managers to own a company such as Oracle (which isn’t listed on the Nasdaq)—and it also means the ETF can own Amazon (which technically is a consumer company).

The ETF is slightly overweight stocks in the portfolio with the best price momentum. As most traders intuitively know, names that are going up tend to keep going up, until they reach a pivot point.

Of course, some of the stocks owned by the ETF may at times lack momentum. In these situations, KQQQ writes call options, which can generate potential income for the ETF—and may be distributed to investors on a tax-advantaged basis.

The ability to write covered calls against portfolio holdings becomes arguably even more important when equity markets experience sharp selloffs. In these episodes, the ETF writes call options against every name in the portfolio, providing some measure of downside mitigation for investors. With market corrections comes higher options premiums (due to a rise in implied volatility), further enhancing the potential income received by KQQQ.

Many income investors shy away from tech stocks, as dividends are either paltry or non-existent. As a result, these individuals end up owning ‘old economy’ stocks in the financial, energy, or utility sectors. In the process they end up sacrificing the growth that comes from tech stocks.

KQQQ can help solve this problem. Investors can have their cake (access to growth companies) and eat it, too (seek income). In the current environment where geopolitical factors are heavily influencing large cap tech stocks, we think this is a wise approach for investors who want access to the potential long-term benefits these companies offer.

Glossary:

Basis Points: A unit used to measure changes in percentages, especially in finance.

Call Options: A type of financial contract that gives the buyer the right (but not the obligation) to buy an asset (like a stock) at a fixed price (strike price) within a certain time period.

Covered Calls: An options strategy where an investor owns a stock and sells call options on that same stock.

Important Information:

The foregoing is general market and economic commentary prepared by Kurv investment professionals as of 04/07/2026. The commentary is neither to be construed as general investment advice nor personalized investment advice. Our commentary is subject to change based upon our views of market, economic, political and related factors. We are under no obligation to provide updated commentary if our views change. To the extent the commentary covers market segments, market sectors, industries, commodities or other securities please note that Kurv professionals may effect transactions in such market segments, market sectors, industries, and commodities or other securities which presents a conflict of interest. All Kurv investment professionals are subject to the firm’s Code of Ethics policy.

For more information on Kurv Investment Management please visit www.kurvinvest.com.