Zooming Out: The Long-Term View

The long-term trend is underpinned by the nascent debasement trade. Investors recognize that developed world governments have little appetite for reining in elevated deficits. Faced with burgeoning debt-to-GDP levels, countries such as Japan and the U.S. may elect to inflate away their debt burdens. Aiming to protect their purchasing power if this comes to pass, retail and institutional investors have moved into hard assets.

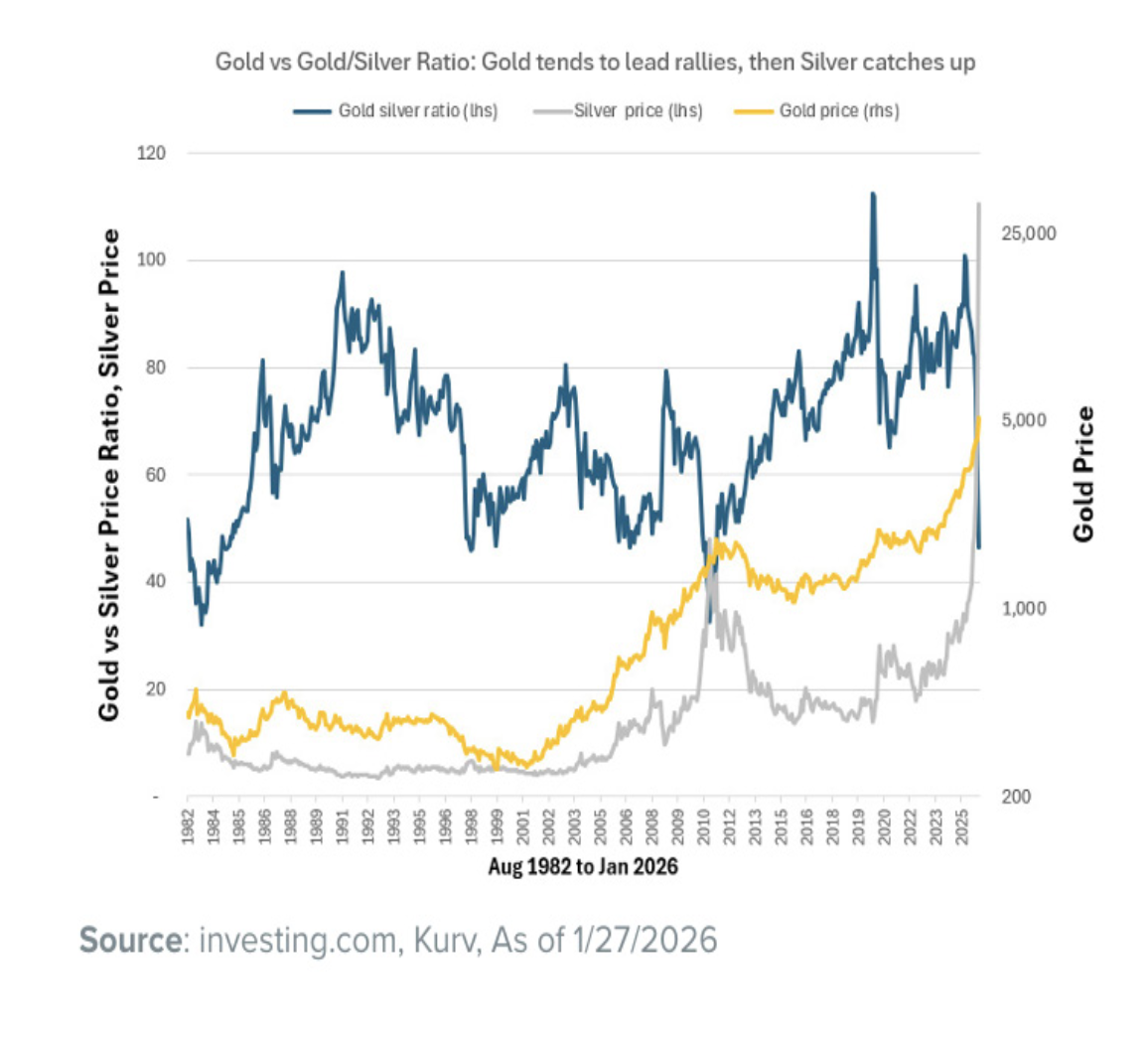

Gold moved first last year as the debasement trade gathered steam. Silver, as it typically does, moved later. Often described as the poor man’s gold, silver tends to play catch-up after the yellow metal has gone on a significant bull run. Case in point: The gold-silver ratio peaked at just over 100 in April. As of February 6, it sits just shy of 64, having reached reached 46 when silver spiked to $120 in late January. From a historical standpoint there is potential scope for further out performance, too: In the 2011 silver bull market, the gold-silver ratio touched 32.

Silver’s bullish long-term outlook is also influenced by its role as an industrial commodity in addition to its status as a precious metal. According to the Silver Institute, 2025 provisionally saw a deficit of around 95 million ounces. (For context, demand was on the order of 1.1 billion ounces).

Zooming In: Short-Term Considerations

Technical factors appear to be playing a central role in the short run for silver. First, there is a significant variation in prices depending on location (i.e. there is not one global silver price). Spot silver in Shanghai has recently traded at a $10-$15 premium over both London and New York, possibly due to export controls announced in late December by the Chinese government. This divergence creates a short-term arbitrage opportunity as traders buy in London and New York and ship to Shanghai. Of course, these arbitrage trades end up draining inventories in the West and contribute to ongoing silver squeezes.

It’s important to note that the wild moves we’ve seen in silver in the last few months do not appear to be based on speculation in the futures market. Indeed, the COMEX raised margin requirements multiple times in December.

In effect, what we normally think about as speculators are morphing into investors given the capital required to stay on the long side. (And if hiking margin requirements does cause speculators to flee, that would simply exacerbate the difference between COMEX and Shanghai, further encouraging arbitrage trades).

That detail aside, the fact remains that net managed money (i.e. hedge fund) silver long positions are nowhere near exuberant. Not only does this suggest that futures markets are not driving the bullish bus, it also raises the possibility that should a speculative bandwagon develop, there’s significant fuel to the upside waiting to be spent.

Typically, only 2% of silver futures holders stand for delivery. Should this figure increase substantially, that may pose a problem for the integrity of the market if there is not adequate supply to satisfy delivery demands. Perhaps investors may come to regard London and Shanghai as representatives of the true silver price, making COMEX less relevant in the process.

How the Long and Short Term Intersect

What connects short-term arbitrage trades in silver with the long-term bullish outlook? In our view, there is simply not enough physical to go around given high levels of demand from both industrial and investment players. We see this dynamic manifesting itself in regional shortages, which then result in higher prices vis a vis other key trading venues. Arbitrage trades take advantage of these discrepancies, creating shortages in other parts of the world.

It’s possible to imagine bearish factors imposing themselves on silver in the medium term . At a high enough price, we could see meaningful substitution to copper. Meanwhile, a stronger U.S. dollar or higher real yields could also weigh on silver prices.

These bearish risks, while possible, do not seem imminent. And in any case, they likely won’t dent the debasement trade, nor resolve the gaping deficit at the heart of silver’s current bull market.

Important Information:

The foregoing is general market and economic commentary prepared by Kurv investment professionals as of 01/26/2026. The commentary is neither to be construed as general investment advice nor personalized investment advice. Our commentary is subject to change based upon our views of market, economic, political and related factors. We are under no obligation to provide updated commentary if our views change. To the extent the commentary covers market segments, market sectors, industries, commodities or other securities please note that Kurv professionals may effect transactions in such market segments, market sectors, industries, and commodities or other securities which presents a conflict of interest. All Kurv investment professionals are subject to the firm’s Code of Ethics policy.

For more information on Kurv Investment Management please visit www.kurvinvest.com.